Vicky bro, Yamaha ki to wapsi ka sun rahe hein hum (per 2015 tak time lag jae ga). +biker community mein se limited log internet use karte hein and are aware of technology. Baqi 65%+ population dont have access to internet nor they understand technology updates. For them brand works. As i myself now a days posted in a rural area, here brand psychology works from ages... Top Honda phir suzuki and few people here abi tak DYL ko Yamaha samajh lete hein and dhoom/Junoon liye ghomte hein. Chonda wo log le lete hein in these areas who cant afford honda/suzuki ya phir ager koi school going student farmaish kar de to use le dete hein. so phychy here is quite different than city....

Technology ke sath sath clean sweep karne ke liye RP and doosre brands ko is customer line ko engage karne k liye bi marketing strategy/policy banai ho gi. Warna AHL ko out karna itna asaan nahi he. is brand k die hard fans (who are not techno/net guys) ko torna is not that easy.

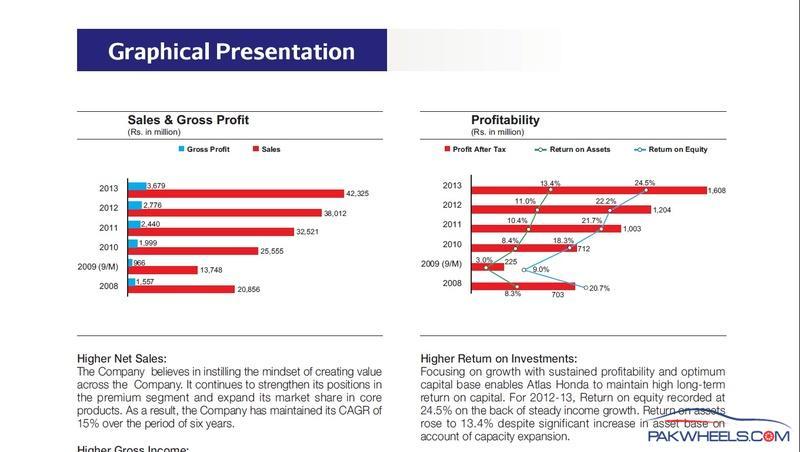

Some statistics for AHL financial picture in FY12-13(Source: http://www.brecorder.com/company-news/235/1264845/):

Performance Review, FY12 During the period under consideration, the company's top line posted an impressive growth of 17 percent and attained an unsurpassed sales figure of 38 billion.

The motorcycle segment touted a staggering growth of 11.1 percent. The company attributes this sales growth to its superior rural penetration as the company believes that the major demand of two-wheeler comes from the remote areas. To cater the rural market effectively, the company has launched smart sales points (SSP) to enhance its presence in the remote areas. Spare parts, the other segment of AHL, though encumbered by forged, smuggled components, garnered 30 percent sales growth for the company with sales tally Rs 2.6 billion.

Despite significant sales growth, the company's gross margin remained strained during the period, hinging at 7.3 percent as against 7.5 percent in FY11, owing to high material prices, Pak Rupee depreciation, high energy cost etc.

During the period, the company's operating expenses surged by 15 percent mainly on the back of huge spending on promotional and advertising activities to derive sales and also because of expansion in dealership network. During the period, the company expanded its dealer network to include 580 dealers as against 470 dealers in FY11.

On the flip side, the other operating income demonstrated a plunge of eight percent. Consequently, the operating profit margin slipped from 4.6 percent to 4.2 percent.

The key striking factor in company's FY12 profit and loss statement is the massive dip of over 87 percent in the financial cost which buttressed the company's bottom line to an enormous extent. In FY12, the company demonstrated the highest ever profit before tax figure of 1.6 billion. Profit after tax also propped up to 1.2 billion, up 20 percent from the previous year which translated into an EPS of 16.74 as against 13.94 in FY11.

The image of financial statistics is taken from AHL annual report and declared financial statement from http://atlashonda.com.pk/wp-content/uploads/2013/05/ahl_annual_report_2013.pdf

regards,