Pakistan Auto: Cash-flows post strong recovery

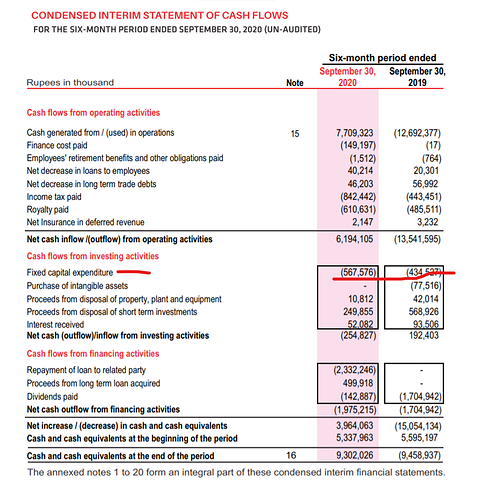

· Presenting an updated cash flow position upon release of detailed financial accounts for auto OEMs we find aggressive normalization in industry CAPEX with the TTM total outlay of PkR5.64bn (down 21%QoQ/60%YoY) with PSMC/INDU/HCAR contributing 23/34/44%,

where HCAR’s CAPEX outlay is an expected indication of model launch expectations.

· The industry’s TTM topline/gross profit recovered from near bottom levels seen just last quarter but remaining lower by 33/48%QoQ where the growth in outgoing Sept’20 quarter was outsized (cumulative sales/gross profit up 2.9x/5.5xQoQ and up 33/62%YoY) showcasing resilience post COVID-19 driven business disruptions while a stable FX situation bolstered margins (industry GM at 6.3% for Sept’20 vs. 5.2% SPLY).

· In terms of free-cash flows, normalized outflows are evident, with net working capital variations improving under healthier order books stabilizing Net Working Capital outflows as the industry rationalized CAPEX (cumulative 2QCY20 CAPEX of PkR5.7bn down 21%QoQ/60%YoY)

· A positive spillover of improved profitability and indication of continued order book health are the drastic decline in leverage levels, as OEMs (led by PSMC) reduce short term loans while benefiting from improved organic cash generation. INDU has filled its ST Invt. coffers back to the brim with current outstanding amount of PkR66.2bn higher than previous peak (PkR55.0bn on June’18) continuing to cushion payouts.