-You can pay upto 70% downpayment.

You have to pay 1st year insurance upfront, last year insurance is paid in installments that's why last year installments are lesser.

Basic payments upfront

Down payment.

Bank charges.

Processing fee.

Taxes (under rs.2000)

Registration charges.

Insurance (2.5-2.75) depending on the company

-2 years is fine. I think banks dont let you finance or lease for less then 2 years.

-Kibor + banks margin varies from bank to bank check with 2 to 3 banks to get the best deal.

-Kibor rate can change after 1 year of finance or lease.

-In case of financing you are the owner of the vehicle in the books and the car shows as your asset in your wealth statement, that is why you pay the withholding tax and can adjust it in your annual returns.

-in case of leasing the owner on the books is the bank. Such a car is rented to you. You pay monthly rentals. It's not shown in your assets until final payment, settlement then the bank sells you the car. That is why the bank pays the withholding tax and adjusts it in there annual returns.

-Islamic banking is similar to leasing, you rent the car from the bank that is why, the bank bears the withholding tax.

-Leasing or Islamic banking is suitable if you want to avoid taxation and the car in your name. In end the of the lease period the bank gives you an NOC. You can sell the car with the NOC and the person purchasing it can get it double transferred from the bank to directly on their name.

I hope it clears. Bank alfalah usually can get you a Toyota / Suzuki car on priority delivery.

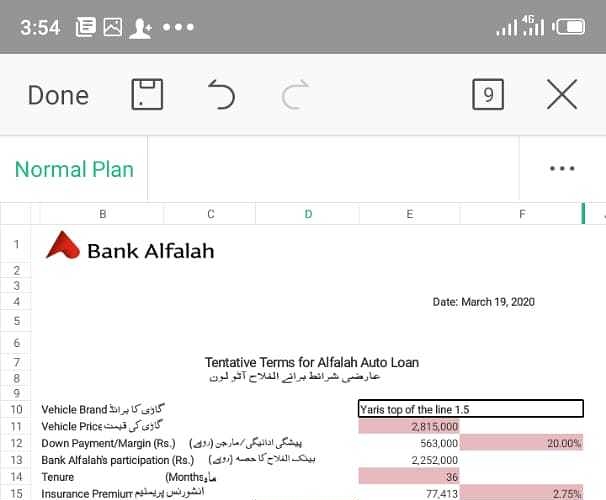

I'm attaching a random screen shot from bank alfalah old rates of Yaris