The {THE SECOND SCHEDULE, EXEMPTIONS AND TAX CONCESSIONS [See section 53] PART I, EXEMPTIONS FROM TOTAL INCOME} gives the rules regarding tax concessions regarding charity and other income eg. pension.

The Second Schedule is on Page 429 of the Income Tax Ordinance 2001 amended upto 31-10-2018 (Available on FBR Website).

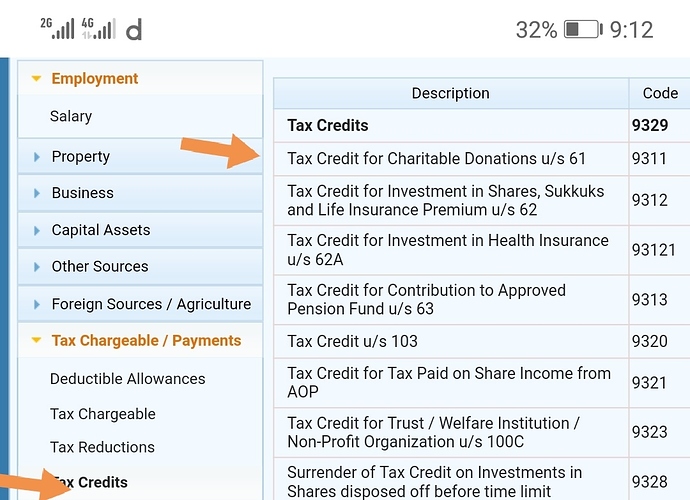

The prescribed charities are mentioned on page 442 of the same Income Tax Ordinance:

[

(61)1[Any] amount paid as donation to the following institution, foundations, societies, boards, trusts and funds, namely: —

(i) any Sports Board or institution recognised by the Federal Government for the purposes of promoting, controlling or regulating any sport or game;

2[(ia) The Citizens Foundation;]

3 Fund for Promotion of Science and Technology in Pakistan;

(iv) Fund for Retarded and Handicapped Children;

(iv) National Trust Fund for the Disabled;

4 Fund for Development of Mazaar of HazaratBurri Imam;

(viii) Rabita-e-Islami's Project for printing copies of the Holy Quran;

(ix) Fatimid Foundation, Karachi;

(x) Al-Shifa Trust;

etc...etc...etc....(plz read the section to go through the complete list).

2[Provided that the amount so donated shall not exceed—

(a) in the case of an individual or association of persons, thirty per cent of the taxable income of the person for the year; and

(b) in the case of a company, 3[twenty] per cent of the taxable income of the person for the year 4[; and] ]

]