Report: Investing in Cars is More Profitable than Fixed Deposits

The most important question for any Pakistani who is looking to make profits out of their savings is, “What should I do with my money?” Majority of the people just opt for fixed deposits because of their consistent yields for a longer period of time and lack of over-complicated predictions, which means majority of the people don’t realize the potential of investment in automobiles in Pakistan.

So, this blog entry is aimed towards comparing the profits yielded by investing the same amount of money in the same timeframe in fixed deposits and automobiles, as this will give the much needed insight into the profit margins of both.

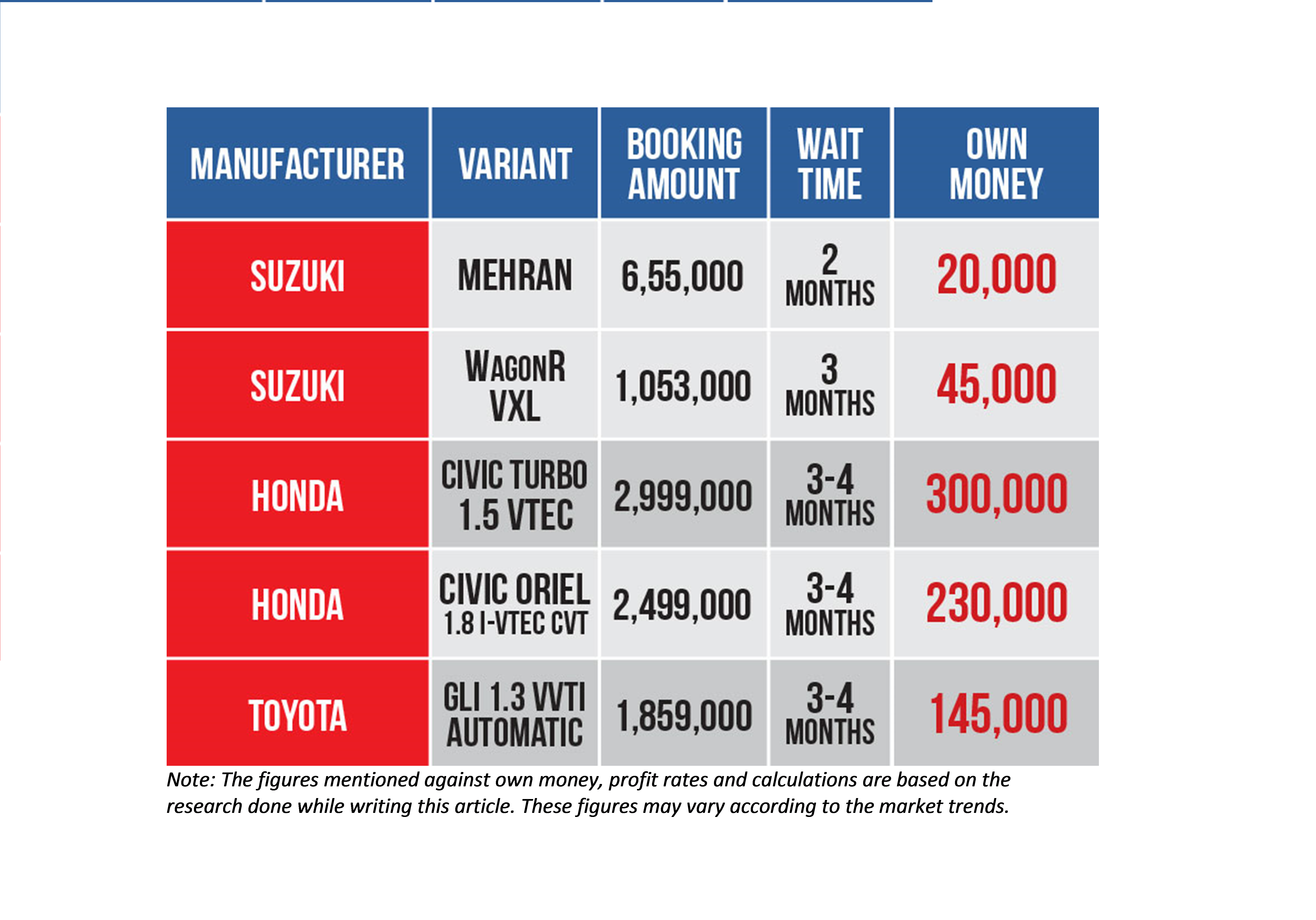

So without further ado, let’s go ahead and have a look at the following list of automobiles, which are very popular in Pakistan.

And for the sake of this blog entry, the list of vehicles has been limited to one variant from each manufacturer. In this case the cars include be Suzuki WagonR, Honda Civic Turbo and Toyota Corolla GLI 1.3 VVTi Automatic.

Here it should be mentioned that the growth of automobile industry is highly regionalized, but these regionalized trends are often accompanied by some quirks in many areas of the world. In Pakistan’s case, we have the example of ‘Own Money’.

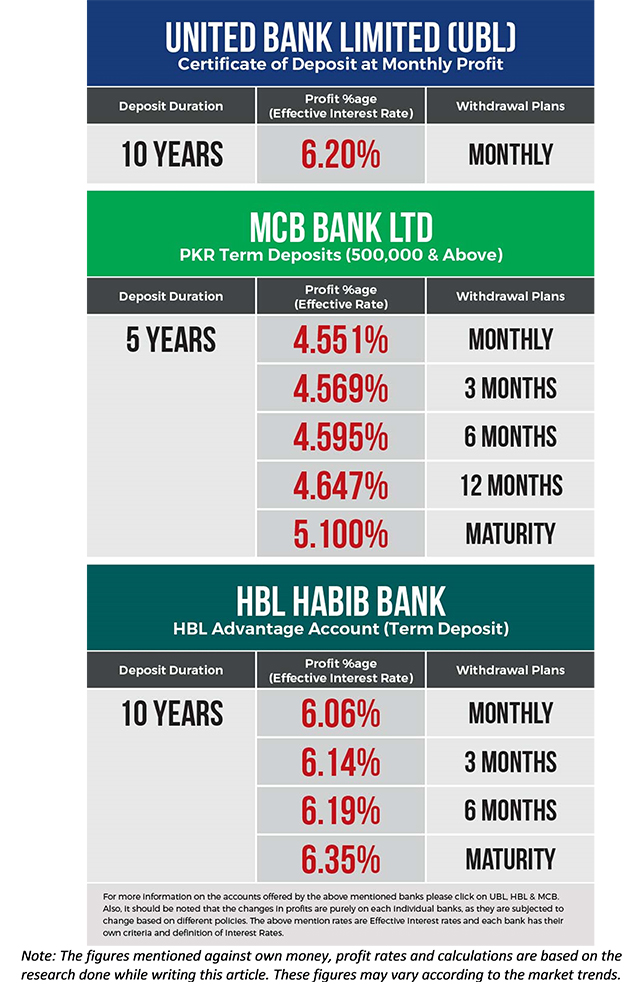

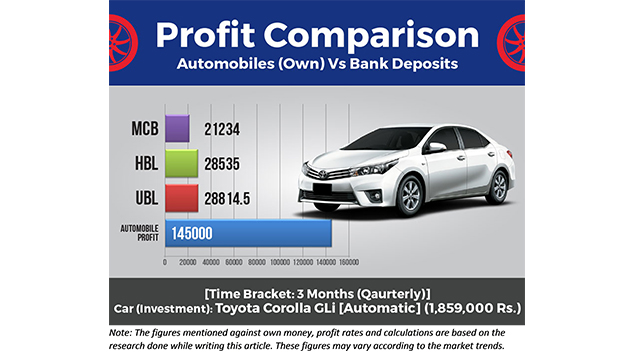

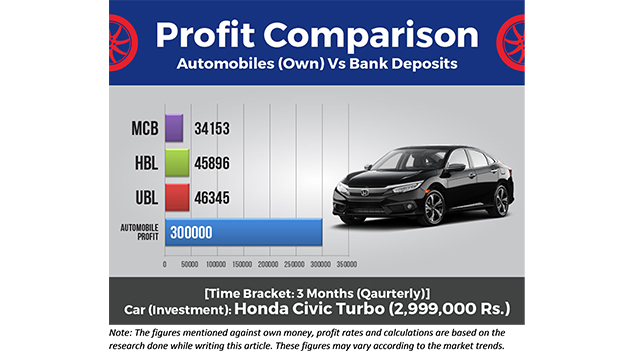

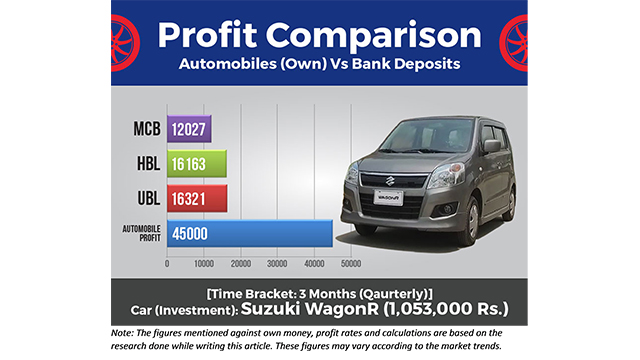

Now that we have our first data sample, we shall have a look at the options, which banks have to offer. So let’s consider country’s 3 of the biggest banks UBL, HBL & MCB, and the fixed deposits for each bank, which yield the highest profits margins. These days, HBL Car Loan Scheme is getting popularity.

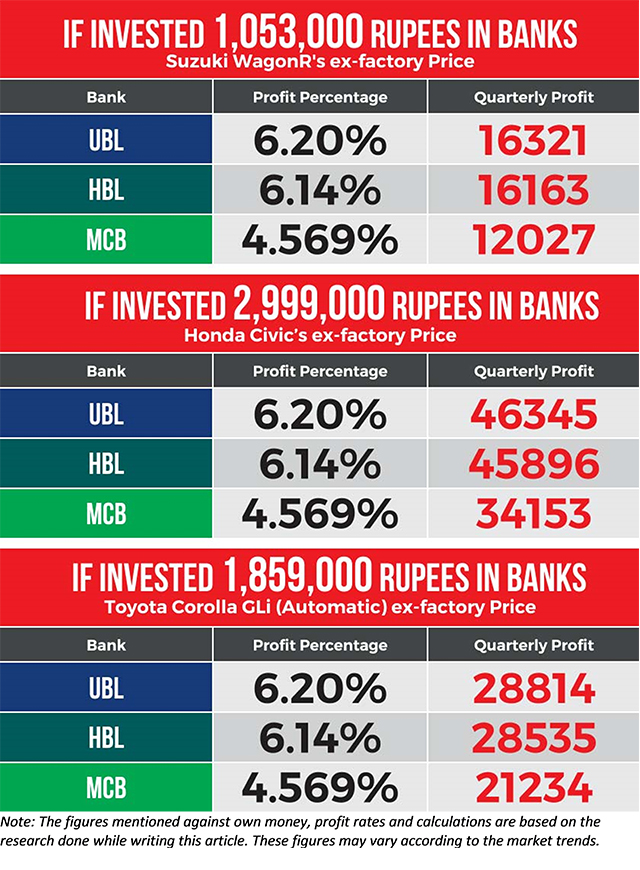

Moreover, our time bracket is 3 months (Quarterly), which will help us to comprehend this data easily.

And now following numbers are the calculated profits of the banks for 3 months fixed deposits on the prices of Suzuki WagonR, Honda Civic Turbo & Toyota Corolla GLi (Automatic).

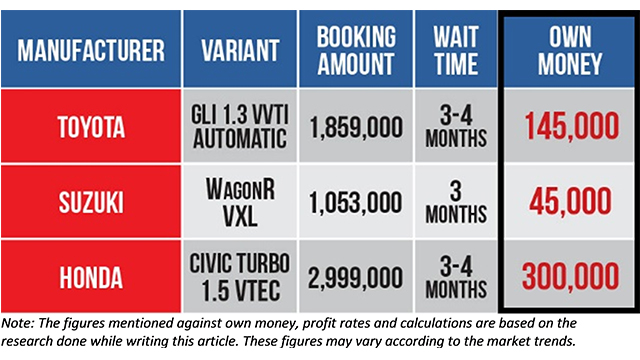

And here is the breakup of automobile profit for the same time bracket off 3 months booking time.

And now let’s just go ahead and put these data samples together, and we will get an idea on the profit returns for both cases.

Those figures are really something to look at. In all three cases, the profit margins of automobiles (cars) far outstrip those of bank deposits, which means more profit yield at the end of three months.

Risk Analysis:

Every investment has some risks associated with it and in the automobile’s case, it can be related to the country’s economic condition, manufacturing throughput and investment security. While the country’s economic conditions will end up affecting both cases in our comparison. Manufacturing throughput on the other hand is inversely proportional to profit in the local automobile industry; this phenomenon is also known as the ‘Demand and Supply of a product’. And as cars are designed to travel on the road, there is always a possibility of accidental damage or a crash. Whereas some banks do offer the safety of investment but the profit return percentage is a subject to change of policies and withdrawal plans.

So, where does this comparison lead us? Although the banks do end up giving consistent profit returns, which are based on the amount, account type and withdrawal plan. The business psychology is naturally more inclined towards the automobile investment as it yields much higher financial gains. Furthermore, why invest money for a longer period of time (5-10 years is the most profit returning in fixed deposits) and continue to receive nominal returns, when instead, the profit from investing in automobiles is significantly higher.

This article was just aimed to shed some light on financial profit yields in two different industries, based on some equal factors. What did you think of this effort?

What’s your opinion on this? Share with us in the comments.

Interesting. Please consider following points:

1. Only conventional banks have been considered, a sizeable chunk of people do not go for conventional banks’ investment options. (Even conventional banks now have Islamic instruments on offer which is worth exploring, however most of the Islamic banking is done through Islamic banks).

2. People investing in financial instruments such as fixed deposits are usually retired age, widows, physically handicapped people, minors (governed by trust); generally people who otherwise cannot run a business venture due to their limitations. It is known fact that business returns are greater than any savings scheme (risk and reward, both are bigger).

3. Are you condoning on-money (own-money)? Pakistan already has a shortage of vehicles, which is cars have a waiting period and on-money associated with them. In this situation in other countries/commodities, there is rationing in which people who want to buy have to justify their need. Granted we do not have such warlike situation and are reaping the fruits of capitalism, but don’t you think is unfair advantage to contribute to the artificially jacking up of prices?

I for one would never buy a car just for “investment” purpose. I’d only buy a car if a intend to use it.

According to the Islamic teachings (as most of the readers are Muslim) too, buying something you would not use yourself is اسراف at the least and ذخیرہ اندوزی at the most, and both are looked down upon. I met some non-Muslims also who have high enough morals that they won’t buy something they can’t use for themselves. In other words, they do not wish to capitalize on the need of someone else.

I forgot one point: one of the risks associated with cars (specially the cars which are new, have high on-money and high resale) is the amount of torture car robbers inflict during the car-snatching.

From what is going around, mobile snatching (from the victim’s POV) is a far better experience compared to car snatching, since mobile snatcher gives their victim a quick death, but car snatchers beat the crap of out the victim before throwing him out. (Him as in, we never came to know of any incident where a car or phone was snatched from a woman. In Pakistan, most women are well-shielded from violent street crime whereas their plight is inside the homes & offices such as domestic violence, honour killings, quid pro quo, but here we are going way off-topic).

Own money business is illegal. This is the reason why waiting time is so long. Genuine buyers have to suffer in the end.

Always shows two side of pictures. how can we get rid off FBR if we booked the car. Secondly withholding tax filer non filer. 3rd delivery time is more the mention here. The showroom charges for sales the vehicle on premium. Currently it is not the right time to invest in auto mobile. Most of the cars(Toyota, Honda, Suzuki) are end of Year. The demand of cars decreased and cars sell on invoice amount rather then own amount.

No wonder Pakistan is still in dark ages.

in business you have to capitalize on the need of others. That is how a business is run. That is how showrooms are run, that is a what “show”room means. You buy (investment) cars, keep them on display for others to buy not for yourself to use

And then there is the definition of “fair business”.

And then there are “fair trade commissions” and “competition commissions” and “consumer courts” in practically every modern country of the world.

Business is about providing a service to the society, not about fleecing them. If only money is on the mind of the businessman, he/she can go ahead and commit robbery.

Of course business being a service does not mean running a not-for-profit venture, neither it means running at 8% profit so that the company fails in the smallest possible downturn. The business needs to be a business, it should not be close to charity, but neither should it be close to robbery.

Otherwise if you think “on money” is fair business and is “fair” capitalizing on other’s needs then why the heck is it illegal? If it was so good, not only it should not be illegal, it should be practically subsidized and encouraged by the government.

————————-

Now let’s compare your idea against the tone of the article.

“Dealer” is a dealer, meant to provide some sales and service under suitable agreement with the manufacturer. It is similar to a shopkeeper who keeps wheat and rice, the quantity is much greater than what the shopkeeper (and his immediate family) can use. But then if the shopkeeper makes/contributes to artificial shortage, what would happen?

On the other hand the article suggests readers to become an “investor”, not a “dealer”. An “investor” is not interested in providing that service to the society which a “dealer” provides. An “investor” is just there to rip others off instead of investing in other options. The agreement between the dealer and manufacturer is legally binding and protects the interest of everybody: the manufacturer, the dealer and the whole society at large. But the “investor” is different, do I get my point across?

The profit Margins shown by the author are not true. the consistent profit margins are:

1. Civic Turbo (a new launch but now at 150K to 175K for investor)

2. Civic 1.8 Oriel ( 100K to 125K )

3. Gli / Gli Auto (80 to 100K)

But yes author is right you still get profit far better than Banks

Own money or on money is illegal – even the government has taken steps to introduce measures (including the new Auto Policy) to end the concept. What you are suggesting is essentially illegal. Plus, the fixed deposits in banks are the lowest form of yield on money being offered. Try looking at other options, like Mutual Funds, stock, treasury bills, PIBs etc. The yield on low / medium risk mutual funds is about 10%-12%, likewise for treasury bills and PIBs which investment banks can purchase for you. On the other hand, stock options have seen yields as high as 40% depending on market conditions and the stock being purchased (refer to IPOs of firms like Engro and Hascol etc) within weeks instead of months but the risk is huge – you can make money in a dramatic fashion or lose it equally dramatically. I haven’t even started on the real estate market – prices can shoot up within a week where premium real estate is involved (refer to DHA City Karachi or Bahria Town Karachi) and yield is more than 200% on the original investment. So ha – ha – ha on ‘investing’ in the automobile sector. The only investment in cars that I see involves rare and vintage cars restored to their original glory or concours level finish and then sold privately or auctioned to collectors.

This is very interesting article, I agree that the banks are giving very low return but I would stay away from booking of new cars. Own money is just like hoarding of sugar, rice etc. Yes its illegal and can be termed as haram.

I would invest in used cars, buy them and resell them which is legal and you get fair return.

Secondly Its just matter of time that FBR will starts targeting non-filers booking new cars.

Interest earning is haram, period.